On 15th July the European Commission will present its proposals for overhauling the EU Emissions Trading System (EU ETS), the most significant regulatory event since the ‘Fit-for-55’ package was launched in July 2021.

Over the following 12-18 months the Commission’s blueprint will be debated by the EU Council and the EU Parliament, and at some point – probably in the second half of 2027 – we will then get a compromise agreeable to all three bodies that will set the operating parameters for the world’s largest and most liquid carbon market well into the next decade. Such is the magnitude of this moment.

So, what are the main changes the Commission is likely to recommend and how controversial are they likely to be? We see five key topics to watch out for, each one being a likely source of heated debate over the next 12-18 months.

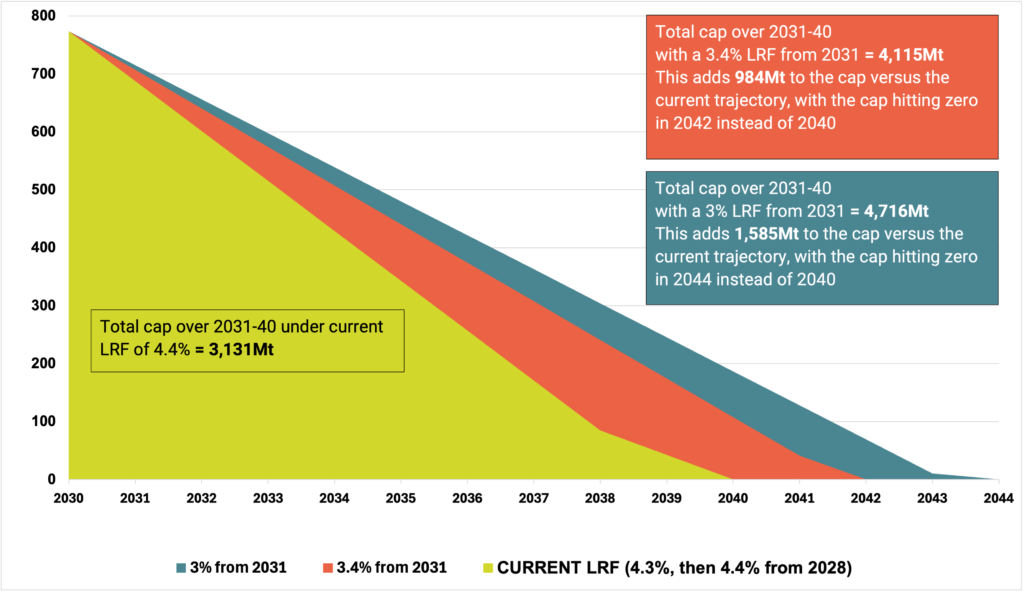

First, the Commission is likely to recommend a reduction in the Linear Reduction Factor (LRF) from 2031 onwards. Under the current legislation the LRF declines at 4.3% over 2024-27, and then at 4.4% from 2028, which means that on the current trajectory the EU ETS cap is set to fall to zero by 2040. However, given the impact of persistently high energy prices over the last five years on both European industrial competitiveness and consumer affordability, this trajectory is no longer politically viable. As a result, we expect the Commission to propose a lower LRF from 2031 onwards, probably between 3% and 3.4%.

Figure 1 shows how an LRF of 3.4% and of 3% from 2031 would compare with the current 4.4%.

Source: European Commission, CLIFI; *For fixed installations only (i.e. excluding Aviation and Maritime)

While the implied increase to the total cap under both an LRF of 3.4% and 3% would be significant, it is important to emphasize that in both cases >70% of the increase versus the current cap would accrue beyond 2035. This means that assuming the Commission proposes the new LRF take effect from 2031, there would not be any meaningful impact on the supply/demand balance in the EU ETS before 2035 anyway, even assuming a significantly lower LRF of 3%. As a result, as long as the Commission does not propose an LRF materially below 3%, and that it proposes that the change to the LRF does not take effect before 2031, we think the LRF proposal will be broadly market neutral as we think a reduction into the range of 3%-3.4% from 2031 is what the market is currently pricing.

Second, the Commission may make further changes to the way in which the Market Stability Reserve (MSR) operates beyond those already announced at the EU Council meeting in March. At the March Council meeting the Commission proposed to cease invalidating allowances in the MSR above the 400m threshold from the end of this year, which means that the MSR will start building up a larger surplus very quickly. Modelling this change alone we now project that the MSR will hold 976m EUAs by the end of 2030, versus the 400m it would hold under the existing policy.

In terms of other changes to the MSR that the Commission might propose, the most significant would relate to the thresholds for withholding allowances from auctions (currently set at 833m) and releasing allowances back to the market (currently 400m). Any proposed reduction of the threshold would be bullish for the market, but we think that when combined with an end to invalidation from the end of this year the current MSR parameters already mean that the Commission will have greatly increased flexibility for dealing with any future price spikes.

As a result, we think the most likely change the Commission will propose to the MSR thresholds is a reduction in line with whatever revised LRF it ends up proposing. We do not expect the Commission to propose any change to the current intake rate of 24%, but if it puts forward a reduction to 12% – the original number it suggested when the MSR was first debated in 2017 – then that would be bearish.

Third, there is the question of the so-called Investment Booster (IB). The Commission has already said it wants to raise €30bn for industrial-decarbonization purposes from auctioning 400m EUAs, but it is not yet clear where those EUAs will be sourced from nor over what timeframe the auctioning will take place. In our view, the most likely source of the 400m allowances is the New Entrant Reserve (NER), which currently holds just over 500m EUAs.

As far as the timeframe is concerned, we assume that the Commission will propose that the 400m allowances be monetized gradually over the five years 2028-32 as 2028 is the earliest date from which the auction process could begin. The Commission has already said that it does not want the auction process for the IB to have a negative impact on prices, and its target of €30bn implies an average auction price of €75/tonne (very close to current levels). Accordingly, we think the Commission will be wary of an accelerated auction process of less than five years, as the higher annual volumes implied by a shorter process would risk crashing the EUA price.

Fourth, there is the question of what to do about the Aviation sector: will the Commission propose that all flights departing the EU be included in the EU ETS, or will it give the Carbon Offsetting and Reduction Scheme for Aviation (CORSIA) more time to prove that the global aviation industry can deliver meaningful emissions reductions in line with the Paris Agreement? We think bringing departing flights back under the scope of the EU ETS would be very difficult to enforce in practice as it would be opposed by major countries such as the US, China, Russia, and India. Moreover, and as a result of this international opposition, certain key EU countries such as Germany and France are also against it. Nonetheless, the Commission may at this stage propose that all departing flights be included in the EU ETS for use as a bargaining chip with the member states on some of the other issues.

Finally, there is the question of whether the Commission will propose that a limited quota of Article-6 credits be allowed for use in the EU ETS. Given that the EU has already agreed to allowing up to 5% of its 2040 emissions-reduction target to be met via international credits, it is possible that the Commission will propose that part of this overall quota be allowed for the EU ETS. However, we think the Commission is philosophically opposed to allowing international credits back into the EU ETS – Commission spokespersons frequently cite the experience with Kyoto credits over 2008-20 as being negative – and we therefore expect it not to propose any use of Article-6 credits in the EU ETS.

That said, we think a number of member states are very much in favour of allowing Article-6 credits into the EU ETS and that as a result this will prove one of the most hotly contested elements of the entire EU ETS Review.

In short, it is time to buckle up: we are set for the most significant regulatory proposal in carbon markets for five years in July, and then a long-running debate with many complex technical and political perspectives to be balanced before a final outcome is reached at some point in late 2027.